The Psychology of Saving: Why Some People Struggle

Saving money sounds simple. Spend less than you earn. Put the difference aside. Repeat.

So why do so many intelligent, capable adults struggle with it?

If personal finance were purely mathematical, budgeting apps would have solved everything by now. But money isn’t just numbers on a screen. It’s emotion. Identity. Childhood conditioning. Social comparison. Fear. Hope. Sometimes even rebellion.

The psychology of saving is messy - and deeply human.

Why Saving Money Isn’t Just About Discipline

Here’s a hot take: most people don’t have a spending problem. They have a psychology problem.

Think about it. Two individuals earn the same salary. One builds a safety net within a year. The other lives paycheck to paycheck. Same income. Different behavior. What changed?

Behavioral science shows that financial habits are shaped by internal drivers like:

- Emotional regulation

- Impulse control

- Future orientation

- Core values

- Stress response patterns

Saving money requires delayed gratification. And delayed gratification is like a muscle. Some people were trained early. Others weren’t.

Honestly, expecting everyone to approach money rationally is like expecting everyone to run a marathon without training. Technically possible. Realistically? Rare.

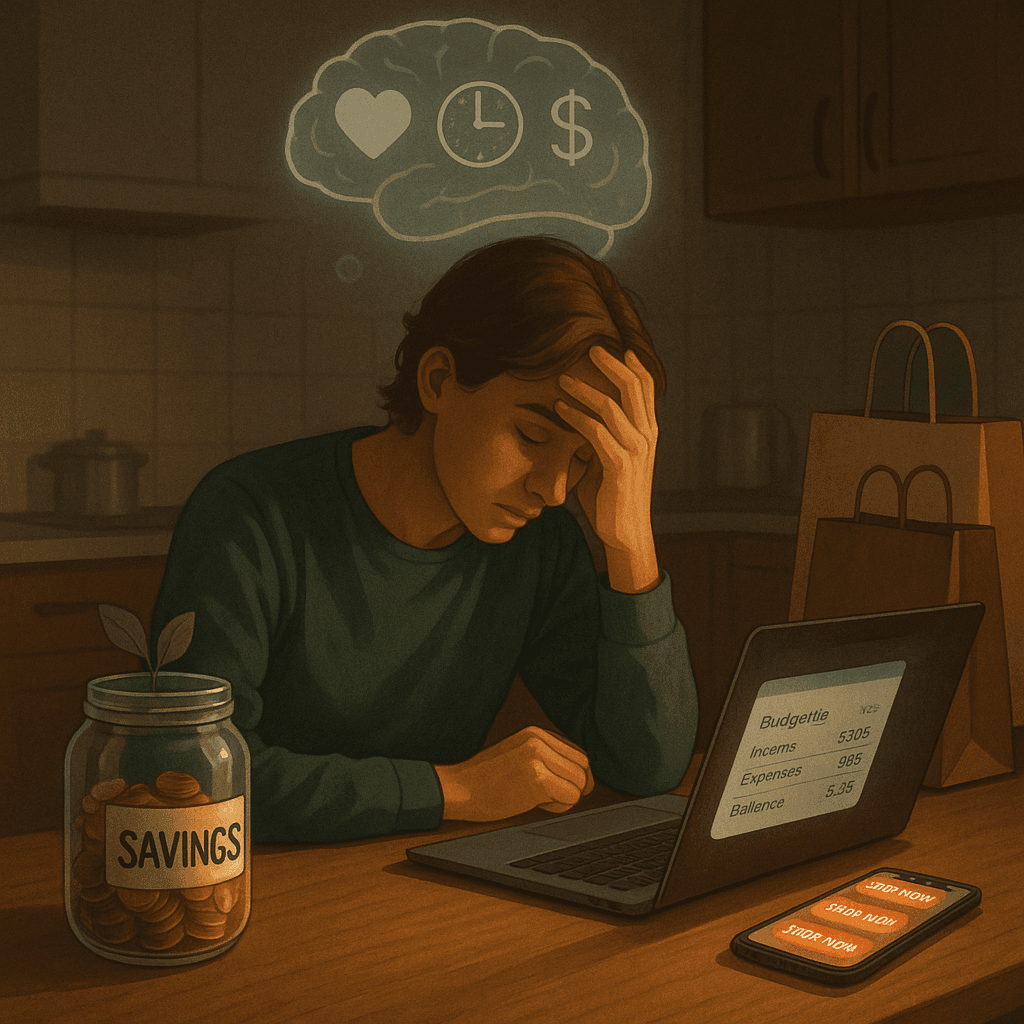

The Emotional Triggers Behind Spending

1. Spending as Emotional Relief

For many, buying something provides a quick dopamine hit. A bad day at work? Add to cart. Feeling overlooked? New shoes. Lonely? Late-night online shopping.

It’s not about the item. It’s about relief.

The brain associates spending with comfort. Over time, this loop becomes automatic. Stress → Purchase → Temporary relief → Regret → Repeat.

Sounds familiar?

2. Identity and Self-Worth

Money is tangled up with identity. Some people save because security defines them. Others spend because status defines them.

If someone unconsciously believes success equals visible wealth, they may prioritize looking successful over building actual reserves. Social media doesn’t help. It turns lifestyles into highlight reels, nudging comparison every five minutes.

Saving, in contrast, is invisible. Quiet. No applause.

3. Scarcity Mindset

Paradoxically, people who grew up with financial instability sometimes struggle the most with saving. A scarcity mindset whispers, “Money won’t last anyway.”

When the future feels uncertain, immediate consumption feels rational. Why save for tomorrow if tomorrow doesn’t feel guaranteed?

This isn’t irresponsibility. It’s psychology shaped by experience.

Personality Traits and Saving Behavior

Not everyone is wired the same way. Personality influences financial decisions more than most realize.

Research across established psychological models highlights patterns:

- High conscientiousness often correlates with structured saving habits.

- High extraversion may increase social spending.

- Low emotional regulation can lead to impulsive purchases.

- Strong intrinsic motivation supports long-term financial planning.

Understanding these traits can be eye-opening. Tools like lifematika.com help individuals uncover behavioral patterns through a comprehensive 95-question psychometric assessment. In about 15 minutes, users receive a detailed analysis grounded in eight established psychological frameworks - including the Big Five, Jungian typology, DISC, emotional intelligence, motivational theory, and more.

Why does that matter for saving money?

Because self-awareness changes strategy. A person high in impulsivity needs guardrails, not just goals. Someone driven by values might save more effectively when linking finances to personal meaning rather than abstract numbers.

One-size-fits-all budgeting advice rarely works because people aren’t one-size-fits-all.

The Future Self Problem

Have you ever noticed how easy it is to promise that “future you” will handle things?

Psychologists call this temporal discounting. The brain discounts future rewards in favor of immediate pleasure. Future benefits feel blurry, almost fictional.

Savings accounts compete against today’s cravings. And today usually wins.

It’s like choosing between a slice of cake now or better health in 10 years. The cake is tangible. The health outcome? Abstract.

People who successfully save often have a strong psychological connection to their future selves. They visualize it. They personalize it. They feel responsible for it.

Without that connection, saving feels like sacrifice without reward.

Motivation Types Matter More Than You Think

Not all motivation is equal.

According to self-determination theory, there’s intrinsic motivation - driven by internal values - and extrinsic motivation - driven by external rewards or pressure.

Someone saving purely out of fear (“I don’t want to be broke”) may struggle to sustain the habit. Fear burns hot but short.

Contrast that with someone who sees saving as aligned with independence, freedom, or responsibility. That’s internal fuel. It lasts longer.

Understanding personal motivational drivers - something platforms like lifematika.com analyze in depth - can shift financial behavior from forced discipline to intentional action.

The Social Influence Trap

Humans are wired for belonging. That wiring doesn’t disappear when money enters the picture.

Consider these subtle pressures:

- Keeping up with peers’ lifestyles

- Splitting bills beyond comfort level

- Buying gifts to signal care or status

- Participating in costly experiences to avoid missing out

Saving sometimes requires social friction. Saying no. Opting out. Choosing long-term stability over short-term approval.

That’s psychologically uncomfortable.

If belonging is a core value, financial restraint can feel like social risk. And the brain hates social risk more than financial risk.

Emotional Intelligence and Money Decisions

Emotional intelligence plays a surprisingly large role in financial behavior.

People with strong emotional awareness can:

- Recognize stress-triggered spending

- Pause before impulse purchases

- Tolerate discomfort without numbing it through consumption

- Separate temporary emotion from permanent decision

Without emotional regulation, budgeting becomes a battlefield. Every craving feels urgent. Every sale feels necessary.

Developing emotional awareness doesn’t eliminate desire. It creates space between urge and action. And in that space, savings grow.

Practical Steps Rooted in Psychology

Instead of generic advice, consider psychologically informed strategies:

1. Automate Decisions

Reduce reliance on willpower. Automatic transfers remove the daily mental negotiation.

2. Rename Your Savings Account

"Emergency Fund" feels abstract. "Freedom Fund" feels powerful. Language shapes emotion.

3. Track Emotional Triggers

Notice patterns. Is spending highest after conflict? Boredom? Social comparison?

4. Align Saving With Identity

Instead of "I should save," shift to "I am becoming someone who builds stability." Identity-based habits stick.

5. Reassess After Major Life Events

Personality and motivation shift over time. Retaking a structured psychological assessment periodically - such as the one offered by lifematika.com - can reveal evolving drivers and blind spots.

Why Some People Change - and Others Don’t

Change requires awareness, emotional readiness, and a strategy that fits personality.

When advice clashes with identity, resistance wins. When strategies align with internal wiring, progress feels natural.

Saving money is less like flipping a switch and more like steering a ship. Small course corrections matter. But first, the captain needs a map.

Self-knowledge provides that map.

The Real Question

So here’s the deeper question: is the struggle about money - or about understanding oneself?

Financial habits mirror psychological patterns. Impulse control. Emotional coping. Long-term vision. Core values. Social needs.

When people explore those layers honestly, saving transforms from restriction into strategy.

And maybe that’s the shift that matters most.

Not tighter budgets. Not harsher self-criticism.

Just clearer insight.

Because once someone understands why they struggle, they’re no longer fighting blindly. They’re adjusting with intention.

That’s not just financial growth.

That’s psychological growth.